Extreme weather

A changing climate: what impact does this have on P&C insurers?

Melchior Mattens MSc AAG

melchior.mattens@arcturus.nl

Now that 2018 has become one of the driest years in the Netherlands since the start of the precipitation measurements and record temperatures are measured worldwide, insight into climate risks is becoming increasingly urgent for insurers. Each type of insurer is affected differently by the warming climate. More drought, extreme precipitation, heat, cold, hail, lightning and wind storm, not to forget the elevated sea level: all these natural phenomena disturb the stability in claims patterns in various ways. But exactly what effects should a non-life insurer in the Netherlands take into account?

Melchior Mattens MSc AAG

melchior.mattens@arcturus.nl

1. NON-LIFE INSURERS – BUILDINGS, LANDS & CARS

The KNMI uses climate scenarios to translate which effects can be expected for the Netherlands in the medium and long term. The most glaring weather phenomena relevant to damage to property like buildings and cars are storms, hail and extreme rainfall and temperature rise. I will discuss these phenomena one by one. In a warming climate, the likelihood of extreme rainfall intensities, where more rain falls in one or a few hours than drain and soil can absorb. In areas with a relatively low natural absorption capacity (like in urban areas) or in areas where water can accumulate due to funneling (for example in hilly areas), the risks for insurers will increase significantly. In addition, large amounts of rainwater in neighboring countries can lead to a higher frequency of flooding in flood plains and villages and cities close to rivers. However, in many cases these losses are not insured, which means that this does not pose a great risk for most insurers. The same applies to the rise in sea level, because a possible major dike breach is uninsurable in the Netherlands.

The risk of extreme hail also increases. Heat can create stronger and more humid air currents, which can make hailstones much larger than before. Larger hailstones not only have an impact because of the larger surface that is hit by the stones, but the greater weight also increases the speed. This can severely damage the roofs of houses and cars. The extreme hail of June 23, 2016 in the southeast of the Netherlands is an example of this, but also on May 29, 2018, hailstones fell in Utrecht, among others, with a diameter of 3 cm – the size of a golf ball. That large hailstones can fall anywhere in the Netherlands is proven by the observations registered in the European Severe Weather Database (see figure below). Most observations of larger hail are in the east and southeast of the Netherlands.

Places in the Netherlands where hail with a diameter of at least 2 cm has fallen since 2006. Source: European Severe Weather Database

Risks for insurers also increase significantly when storms become more frequent and intense. Based on the IPCC report from 2013 and the climate scenarios made by KNMI, it could not be stated with certainty whether storm conditions – with regard to winter storms – for northwestern Europe would change significantly in the coming decades. It is true that the force of local wind extremes is increasing during thunderstorms, for example (also consider whirlwinds and even tornadoes), but due to more buildings in the Netherlands, the average wind speed above land has actually decreased slightly in recent decades. In addition, there are also recent reports from climate and weather scientists showing that the likelihood that powerful tropical storms can reach the Western European coast will increase in a warmer climate.

Then there are the consequences of a rise in temperature. Higher temperatures are associated with more frequent and stronger thunderstorms, which can burn down buildings. This increases fire risk for non-life insurers. However, the likelihood of this culminating in a catastrophe seems limited, even though small insurers can experience a considerably more volatile claims burden when large objects are hit.

A claims source for which Solvency II is currently not yet equipped is the great natural fire risk that can arise from forest fires, for example. Insurers do hold capital for the man-made Fire Catastrophe risk, where all capital is lost in a circle with a radius of 200 meters. However, the likelihood of a large material loss due to large contiguous areas of nature and forest and adjacent villages / cities being (partly) lost also increases. During dry periods with relatively strong winds, forest fires in Europe increasingly appear to be barely or not manageable. This results in great material and unfortunately also human losses. Until now, this has mainly been limited to the southern EU member states, but a country like Sweden also experienced the largest forest fires in its history in 2018. In a warmer climate, the risk of drought – and thus the drying out of soil and vegetation – will also increase in the Netherlands, with a greater chance of wildfires as a result.

Rain, hail, drought and storm are expected to influence the damage burden in different ways. For rain and hail it is quite clear that frequency and strength will increase significantly in the coming decades. This changes both the average and the catastrophe damage burden. Especially the hailstorms with major damage as a result can push the premium up considerably in the Netherlands. This is less clear for storms and droughts. There could be a more frequent autumn storm and drought – if it lasts long enough – could lead to greater damage to nature and property. It is not yet clear whether the insurance premium will be structurally higher as a result.

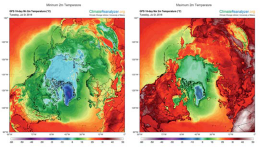

Minimum- en maximumtemperatuur voor poolgebied, Noord-Amerika, Europa en Rusland – 10-daagse projectie vanaf 24 juli 2018. Record hitte in California (>50oC), Noordelijk Afrika (Algerije >50oC), Japan en Korea (>40oC) en noordelijk Scandinavië (>30oC). Bron: University of Maine (ClimateReanalyzer.org)

2. NON-INSURERS – AGRICULTURE

Likewise, for non-life insurers active in agricultural business, hail, rain and storm are risks that can lead to extensive damage to crops. The described risk of wildfires and drought takes on a different form for agri-insurers. Farmers are often allowed to use little or no natural water resources when drought persists for a longer period of time. As a result, a large part of the harvest can be lost in extremely dry years. Under a ‘broad weather coverage’, insured parties can submit a claim for damage caused by loss of harvest in the event of rainfall shortages – as measured by the KNMI – above a set limit.

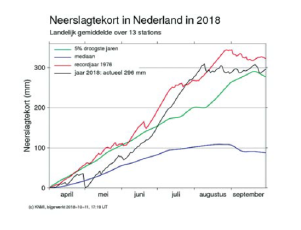

It is now clear that the drought in the summer of 2018 is comparable to the drought in 1976. Drought in the Netherlands is also a sign of climate change. Based on the climate scenarios and analysis of drought periods since 1900, the KNMI states that no pattern can yet be found in the frequency and duration of drought periods.

Average nationwide precipitation deficit as measured in 2018. Source: KNMI

The air pressure pattern that keeps rain away is even slightly less common in the Netherlands after 1979 than before. However, the KNMI also states that climate models show more drought when the dehydration of soil and vegetation in the Netherlands – partly due to higher temperatures – becomes more comparable to the Mediterranean area. With the (probably) four hottest years in a row (2015-2018) since the measurements started in 1900, this is starting to become an increasingly likely scenario. For the insurance business with insured agriculture, forestry and fruit cultivation, it is expected that extreme precipitation from rain and hail can strongly influence the premium. The catastrophe scenarios will also deteriorate considerably. However, with regard to drought, it is still the question whether the frequency will increase significantly.

OVERVIEW

Long-term trends of higher average claims and more extreme catastrophes have a direct impact on insurers’ pricing, underwriting and capital policy. In addition, a demand may arise for new types of insurance where the insurer can meet a social need with more prevention measures and advice.